Martin Lewis has warned about it for years, and it flares up right when you’re most vulnerable: the moment you hit “Pay now” with a debit card. The risk isn’t just the product not turning up — it’s having far less power to get your money back when it does go wrong.

It starts with a familiar scene: a late evening scroll, a slick ad, a discount that ends at midnight. You punch in your debit card details and feel that little fizz of relief — sorted. Days pass, the parcel doesn’t, and the seller’s replies thin out until they vanish entirely. Your bank shrugs, the chat bot loops, and your heart sinks as you realise you’ve essentially paid from your own pocket into a hole. Somewhere in the back of your mind, a line from Martin Lewis echoes about never using a debit card for online shopping. Then the kicker lands.

Why that “never” matters right now

When you pay online, the type of plastic you choose changes everything. Credit cards come with legal muscle in the UK — Section 75 of the Consumer Credit Act — which can make your card provider jointly liable with the retailer on eligible purchases between £100 and £30,000. Debit cards don’t carry that legal shield, and the difference shows up the moment a seller disappears or pushes you in circles. That gap can cost you hundreds.

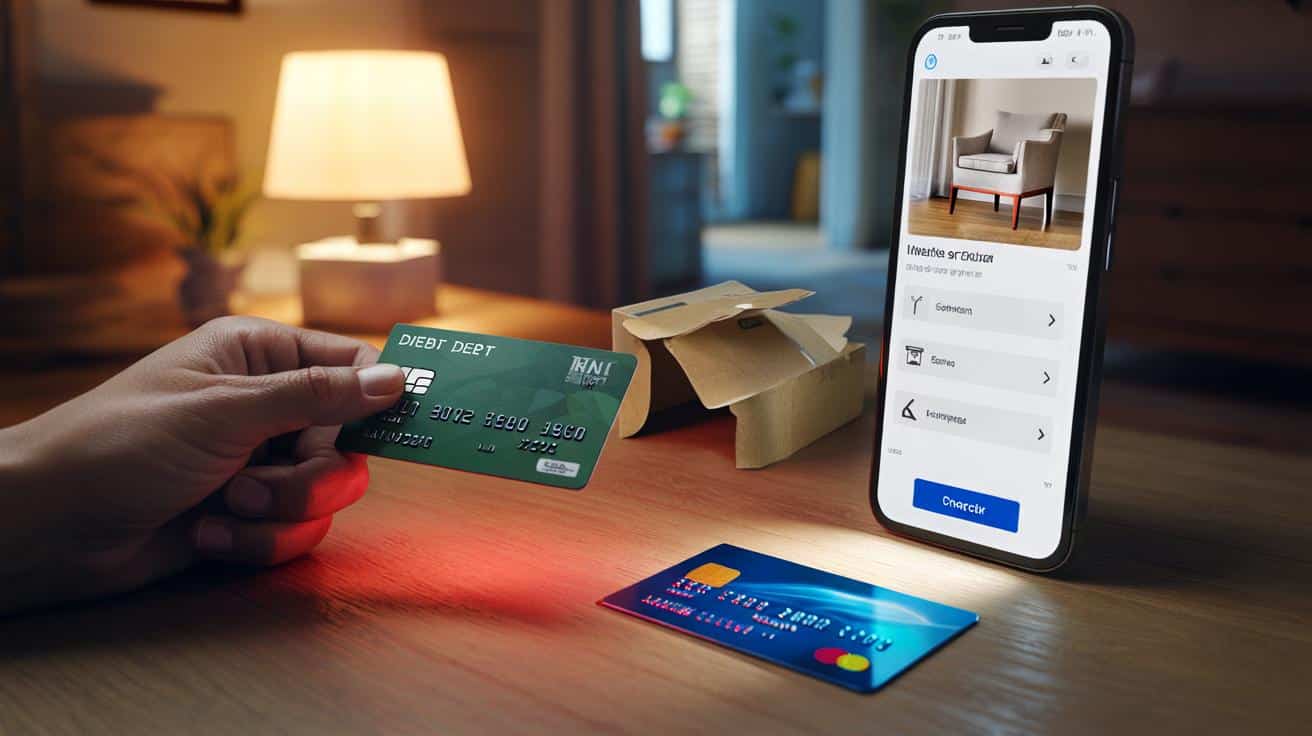

Here’s a real-world shape to it. Sophie orders a £349 armchair from a pop-up furniture site — glossy photos, glowing reviews, and a ticking countdown banner. Weeks later, nothing. With a debit card, she’s relying on “chargeback,” a card-scheme rule where her bank can try to pull the money back, usually within about 120 days of the expected delivery date; it’s not law, the seller can dispute it, and outcomes vary. If she’d used a credit card, she could run a Section 75 claim because the item costs over £100, shifting leverage to the card company that’s on the hook with the retailer.

That legal line is the quiet divide in outcomes. Debit card payments take the money straight from your current account; the bank is a pass-through, not a party to the purchase, so your rights sit on softer ground. With credit cards, the lender is bound into the deal — that’s why Section 75 exists — and it often changes how quickly a case moves and how seriously it’s handled. Your money is either protected by law, or it’s relying on goodwill and admin.

What to do instead (and how to make it painless)

Make a simple split: use a credit card for online buys where there’s any chance of things going wrong — especially anything £100+ or from a seller you don’t fully know — and clear the balance in full each month. Keep one low-limit card just for internet shopping and subscriptions, and park it in your digital wallet so it’s even easier than your debit. If a retailer accepts it, paying with a credit card through a trusted wallet can add extra friction for fraudsters without losing your legal rights. Pay with a credit card and pay it off in full each month.

Watch for habits that quietly void your safety net. Splitting a £500 item across two cards, say £50 on debit and £450 on credit, can tangle Section 75 as it usually hinges on the single item price paid on the credit card. Paying by bank transfer “for a small discount” is basically handing over cash — almost no recourse if things go south. We’ve all had that moment when a deal feels too good to let go; that’s when you need the stronger fallback. Let’s be honest: nobody does this every day.

Think of your purchase like a tiny contract, and keep the paper trail short and tight. Save the product page, the order confirmation, and the expected delivery date; those screenshots are your best friend if you need to claim. Never send a bank transfer to a seller you don’t know.

“Use debit for day-to-day cash withdrawals and confirmed in-person buys; use credit online where you’d need leverage if it all goes wrong.”

- For anything £100–£30,000, a credit card can engage Section 75 if the seller fails.

- Chargeback exists on both debit and credit, but it’s not law and can be challenged.

- Digital wallets are handy, yet the card type behind them still sets your rights.

- Keep evidence: ads, emails, chat logs, delivery promises, and photos of what arrived.

- Start with the retailer, then escalate to your card provider with a clear timeline.

The timing problem — and why this is a “today” issue

Online retail is noisier than ever: seasonal sales, imported goods with long lead times, micro-brands that spin up and vanish, and shiny storefronts built in an afternoon. That unpredictability collides with tighter household budgets and a boom in one-click checkouts where your thumb pays before your brain catches up. A debit card makes that snap feel painless, right until you need to pull the money back and discover you’re negotiating from the weak side.

Fraud isn’t the only risk; shady returns policies, “lost” packages, and promises that slide week by week can drain your time and your balance. Strong Customer Authentication makes it harder for crooks to impersonate you, but it doesn’t turn debit into legal protection. Your choice of card isn’t fussy — it’s practical — because it changes who fights for you when a deal breaks. And when the cost of living squeezes, the last thing you need is a bank dispute that drifts into month three.

If you remember just one thing, let it be this: use debit where the goods are instant and certain, and use credit where you might need a legal lever. Keep that lever close, don’t overthink it, and build a rhythm you can stick to without stress. The difference won’t show on good days — it shows up when you most need a win.

Right now, a lot of online shopping sits in the grey zone between familiar and risky — not outright scams, but murky customer service, weak guarantees, and promises on the edge of believable. That’s why Martin Lewis keeps sounding the same note: your card choice isn’t about fear, it’s about power. When you pick the tool with legal teeth, you get to write the ending. And that ending can be the difference between a shrug and your money back.

| Key Point | Detail | Interest for the reader |

|---|---|---|

| Use credit online for £100–£30,000 items | Section 75 can make the card company jointly liable if the seller fails | Faster, firmer route to refunds on broken or missing orders |

| Debit relies on chargeback | Scheme rule, not law; sellers can dispute and banks can refuse | Know the limits before you’re stuck chasing your money |

| Keep tight evidence | Save ads, confirmations, delivery dates, and photos | Sharper, simpler claims that don’t drag on for months |

FAQ :

- Is it really “never” okay to use a debit card online?For low-value buys from trusted brands, many people do and nothing goes wrong; the point is that you lose the legal muscle Section 75 gives you on a credit card.

- What exactly is Section 75?UK law that can make your credit card provider jointly liable with the retailer for misrepresentation or breach of contract on items costing £100–£30,000.

- Does paying via a digital wallet change my rights?The card behind the wallet sets your rights; use a credit card in the wallet if you want Section 75 on eligible purchases.

- Can I claim on debit card chargeback?Often yes within a set window, but it’s a voluntary scheme rule, not a legal right, and the seller can challenge it.

- What about splitting payment across methods?It can complicate or sink Section 75; paying the whole item price on one credit card keeps the protection cleaner.

Thanks for the clear explainer — I definitly forgot about Section 75 and nearly split a £500 order across cards last week. Setting up a low‑limit credit card just for online buys sounds smart; paying in full each month is key.